Erdal Nuhbasa – Law and Consulting Firm – Legal Services

Erdal Nuhbasa – Law and Consulting Firm – Legal Services

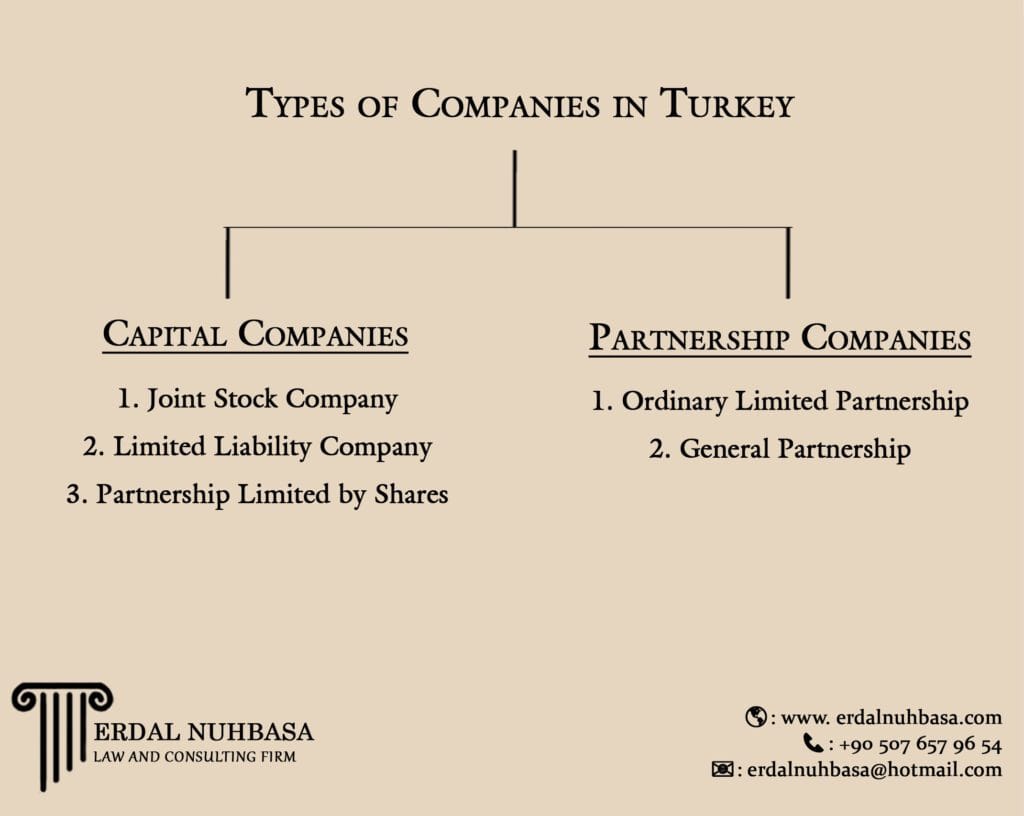

Choosing the right type of company in Turkey depends on your business size, objectives, and future goals. Each company structure offers unique features that cater to different types of entrepreneurs and ventures. By understanding the advantages and limitations of each, you can make an informed decision to support your business’s success.

1. Sole Proprietorship for Simplicity and Control

If you’re an individual looking to start a small business or freelance operation, a sole proprietorship is the simplest choice. It requires minimal paperwork, offers complete control over decision-making, and is cost-effective to establish. However, keep in mind that you will be personally liable for all debts and obligations, which can be a significant risk for high-stakes businesses.

2. Limited Liability Company (LLC) for Small to Medium Businesses

For entrepreneurs planning to scale their business, a limited liability company (Ltd. Şti.) is the most popular option. It provides flexibility with a minimum of one and a maximum of fifty shareholders.

Shareholders’ liability is limited to their capital contributions, offering financial protection. LLCs are well-suited for small and medium-sized businesses, startups, and family-run enterprises due to their cost-effective setup and straightforward management.

3. Joint Stock Company (JSC) for Larger Enterprises

For large-scale businesses, especially those considering raising capital or going public, a joint stock company (A.Ş.) is ideal. It allows for the issuance of shares and provides ease of ownership transfer, making it attractive to investors.

Shareholders’ liability is limited to their shares, reducing personal financial risk. JSCs are commonly used by corporations seeking substantial funding or operating in industries with high investment needs.

4. Specialized Structures: Partnerships, Branches, and Liaison Offices

General partnerships and ordinary limited partnerships are suited for ventures involving close partners with shared responsibilities and trust. They work well for specific, low-risk businesses.

If you are a foreign investor, branch offices provide an opportunity to test the Turkish market while remaining an extension of the parent company. Alternatively, a liaison office is excellent for research or promotional activities without engaging in commercial transactions.

5. Cooperatives for Shared Goals

For groups with shared economic or social objectives, cooperatives are a suitable structure. They are commonly used in sectors such as agriculture, housing, or education, where pooling resources benefits all members.

Cooperatives foster collaboration and ensure shared success, but their collective decision-making process may require additional effort to manage.

Authorized company representatives must sign under the company name, and these signatures must be certified by the trade registry office.

Once your company is established in Turkey, there are several key responsibilities to ensure compliance with local regulations. Registering with the tax office to obtain a tax identification number is essential, along with adhering to corporate income tax, value-added tax (VAT), and other tax obligations. You are required to submit regular tax declarations and register with the Social Security Institution (SGK) to provide social security benefits for employees. Opening a business bank account in the company’s name is also necessary for financial transactions and tax payments.

Engaging a certified public accountant (CPA) or accounting firm is crucial for managing bookkeeping, payroll, and tax filings while maintaining accurate financial records. Employers must comply with labor laws, paying at least the statutory minimum wage and securing work permits for foreign employees.

Any changes in the company’s structure, such as shareholder details, capital, or address, must be reported to the trade registry and, in some cases, published in the Turkish Trade Registry Gazette. For regulated industries, obtaining and maintaining specific licenses is required to operate legally.

Additional obligations include holding annual general assembly meetings for joint-stock companies and submitting financial reports to the trade registry, especially for larger companies. Businesses must comply with competition laws, consumer protection standards, and environmental regulations where applicable. Ensuring adherence to these responsibilities is important for avoiding legal penalties and fostering sustainable operations.